The first three years of the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) were a period when most airlines were not required to buy carbon credits. That changed in 2024, when the scheme produced its first meaningful compliance costs and became an operational reality rather than a policy plan.

CORSIA is on the path to broad mandatory participation in 2027, and the operational picture is completely different from when the framework was established in 2016. The pool of eligible carbon credits is growing, participation has increased, and baselines have been tightened. Here are the ten facts every airline procurement and finance team should have on record.

1. The First Industry-Wide Global Market Measure

In October 2016, all 191 ICAO Member States adopted CORSIA by consensus: the first global market-based measure for an entire industry sector.

That consensus did not mean 191 countries began offsetting on day one. At the launch of the pilot phase in 2021, only about 88 States, accounting for roughly 60% of international air traffic, volunteered to take part.

Participation has increased steadily since, reaching 130 States by January 2026. The real advantage for globally operating carriers: a single international scheme rather than a patchwork of regional ones.

2. Shifting Compliance Baselines

The emissions baseline has changed several times over CORSIA’s development. The original design used the average of 2019 and 2020 emissions, but COVID-19 brought international aviation to a near-standstill in 2020, making that baseline unrepresentative.

ICAO first revised the pilot-phase baseline to 2019 emissions only, then tightened it further for 2024–2035 to 85% of 2019 emissions: more stringent than originally planned, and supported by the industry. Compliance planning depends on these baselines together with future emissions projections, and they are not necessarily final, as a further periodic review is due from 2025 onwards.

3. Airlines Had No Offsetting Obligation Between 2021 and 2023

The pilot phase began in 2021, but airlines paid nothing for three years. Because international aviation emissions were still recovering from the pandemic, ICAO set the sector growth factor at zero for 2021, 2022 and 2023.

This gave airlines time to build monitoring, reporting and verification (MRV) systems before procurement became a requirement. It also meant many procurement teams had little real buying experience before genuine demand arrived in 2024.

4. 2024 Was the First Year Airlines Faced a Real Compliance Bill

ICAO set the 2024 baseline at 305,522,071 tonnes of CO₂, while reported emissions came in at approximately 361 million tonnes. That difference produced a sector growth factor of 15.4% (the first non-zero figure in CORSIA’s history) and a sector-wide offsetting requirement of around 56 million tonnes of CO₂ for the year.

Airlines responded quickly: Singapore Airlines and Japan Airlines were among the first to retire credits against their Phase 1 commitments, turning three years of preparation into a budgeted operational expense.

5. The Cost Curve: From Minor Budget Line to Multi-Billion-Dollar Liability

IATA puts 2024–2026 compliance costs at just 0.07% to 0.15% of total airline operating expense, rising to around $1.7 billion industry-wide in 2026 (up from $1.3 billion in 2025).

Looking further out, in June 2026 the Financial Times reported, citing MSCI Carbon Markets analysis, that the price of eligible-credit supply could rise nearly eight-fold to about $100/tonne by 2035, taking the industry’s cumulative eligible-credit bill as high as $127 billion. Long-haul carriers are the most exposed, with estimates of $8B for Emirates, $6B for Qatar Airways and $5B for United Airlines. Today’s figures describe where the scheme is now, not where it is heading.

6. Not Every ICAO Member State Currently Participates

130 States are participating as of January 2026. From 2027, CORSIA’s second phase requires most States to take part, with exemptions for least developed countries, small island developing States and landlocked developing countries unless they choose to join voluntarily.

CORSIA applies only to eligible routes between participating States, so operators should confirm the specific State pairs in ICAO’s official registry before forecasting obligations.

7. CORSIA Does Not Apply to Domestic Flights

The assumption that CORSIA covers all aviation emissions is incorrect: only eligible international flights count. A flight from London to Paris can fall under CORSIA if both States participate; a flight from London to Manchester (a domestic service) is excluded, regardless of aircraft type or operator. For carriers with mixed domestic and international networks, the overall carbon footprint and the CORSIA obligation can look very different.

8. Carbon Removal Credits Are Now Part of CORSIA

ICAO has approved Isometric as the first carbon-removal registry eligible under CORSIA, allowing airlines to use verified removal units alongside other approved carbon credits. British Airways, the UK’s largest single buyer of carbon removals, welcomed the move, with carbon removals projected to account for roughly a third of its emissions reductions by 2050.

The decision widens the compliance toolkit while upholding ICAO’s approval process. As the number of eligible registries grows, procurement teams increasingly have to weigh programme eligibility and regulatory acceptance alongside price.

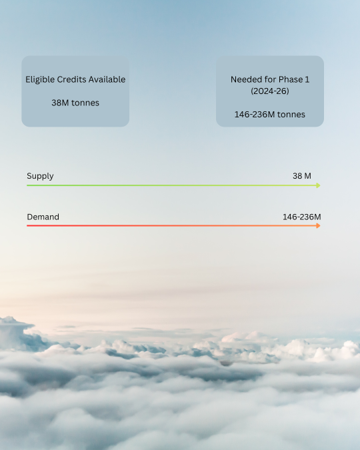

9. The Eligible Credit Supply Gap

Analyst estimates for Phase 1 (2024–2026) demand range widely, from about 146 million to 236 million Eligible Emissions Units (EEUs), with a base case of around 163 million tonnes and up to about 198 million if all participating states enforce in full. Against that, only about 38 million eligible units existed in the market as of June 2026, roughly 23% of base-case demand and a gap of about 125 million tonnes. Even the lowest single-year estimate for 2026 alone exceeds the entire eligible stock available today.

That imbalance is already showing up in pricing, and in the deferred-payment and forward-purchase structures now emerging to help airlines secure volume before the gap widens further.

10. CORSIA Has Strict Rules to Prevent Double Counting

Not every carbon credit qualifies. Eligible credits must meet ICAO’s Emissions Unit Criteria, which require safeguards against double counting against both the airline’s and the host country’s national climate targets. The central element is host-country authorisation, usually a Letter of Authorisation (LoA) backed by a corresponding adjustment under Article 6 of the Paris Agreement.

Provenance matters more than price. If a host country fails to apply a corresponding adjustment under Article 6, even a credit from a premium registry becomes a compliance liability rather than an asset.

What This Means for Airline Procurement Teams

CORSIA has changed significantly since 2016. Baselines have been tightened, participation has grown, and airlines have moved from no offsetting at all to active procurement. The easy years are behind the scheme, not ahead of it.

Eligible supply already falls well short of Phase 1 demand, and price scenarios could push the sector’s cumulative bill into the tens of billions by 2035. The airlines that manage this best will be those that understand how CORSIA actually works, know which credits are genuinely compliant, and have the Letters of Authorisation and documentation in place before a shortfall forces a rushed purchase.

In other words, this is increasingly a procurement decision rather than a compliance afterthought, which is why a growing number of carriers are moving to longer-term carbon-credit procurement strategies built around eligibility, supply security and cost predictability rather than price alone.

Securing CORSIA-Eligible Supply Directly from the Project Developer

This is where sourcing directly from a project developer matters. Econetix is a carbon asset manager that develops and operates its own portfolio of CORSIA-eligible projects across the DRC, Uganda, Rwanda and beyond, and was among the first developers globally to secure Letters of Authorisation for Phase 1 compliance credits. Buying direct from the developer, rather than through an intermediary, gives airlines competitive pricing, delivery guarantees backed by a binding supply obligation, and full traceability through Econetix’s proprietary digital MRV (dMRV) platform. Combined with forward-purchase and deferred-payment structures, it lets procurement teams lock in eligible volume and price today, ahead of a tightening market.

Frequently Asked Questions (FAQs)

Does CORSIA apply to every airline?

No. It applies only to eligible international flights operated between participating ICAO Member States.

Why were airlines not required to buy offsets in 2021–2023?

Emissions were still below the applicable baseline as the sector recovered from COVID-19, so the sector growth factor was zero.

How many countries currently participate in CORSIA?

130 States, as of January 2026.

Can airlines use carbon-removal credits for CORSIA compliance?

Yes. In late 2025, ICAO approved Isometric as the first eligible carbon-removal registry, allowing verified removal units to be used alongside other approved credits.

Why are Letters of Authorisation important?

An LoA confirms that the host country has authorised the credits for CORSIA use and will apply a corresponding adjustment under Article 6, preventing double counting. Without it, a credit is not CORSIA-eligible.

What makes a carbon credit CORSIA-eligible (a CEEU)?

A CORSIA-Eligible Emissions Unit (CEEU) comes from a project under an ICAO-approved programme (such as Gold Standard or Verra), carries a host-country Letter of Authorisation with a corresponding adjustment under Article 6, and is tagged accordingly in the registry. Only credits meeting all of these criteria can be retired against a CORSIA obligation.

Where can airlines buy CORSIA-eligible credits?

Airlines can source CEEUs through traders and intermediaries or directly from project developers. Buying directly from a developer such as Econetix, which owns and operates its CORSIA-eligible portfolio, gives carriers competitive pricing, a binding delivery guarantee and full transparency on provenance and LoA status.